5 min read

Global Commercial Drone Operation Increased by 42% – Prevailing Challenges Limit Stronger Growth

Global Commercial Drone Operation Increased by 42%

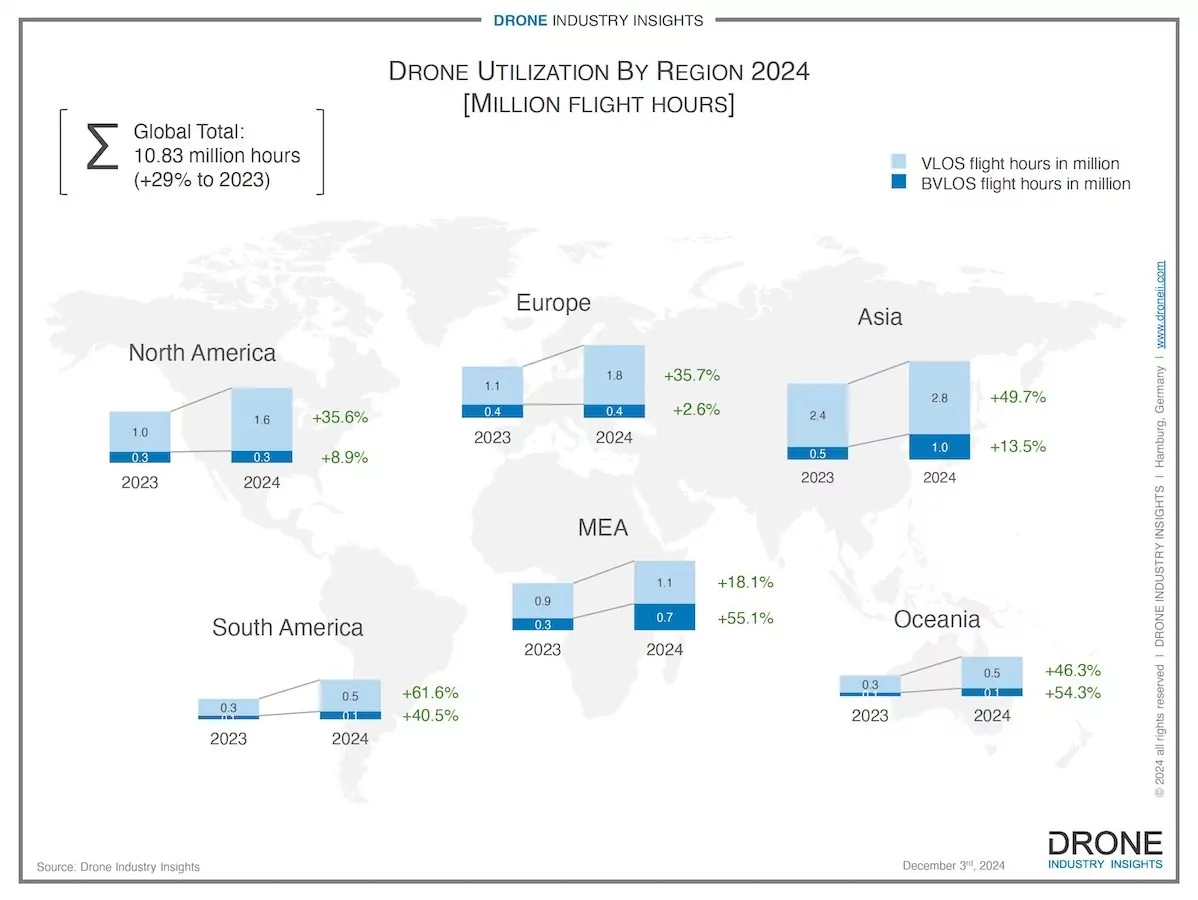

The Global Drone Industry Review 2024 reveals that the drone industry is demonstrating increasing operational sophistication and market specialization. Advanced mission capabilities and complex use cases are becoming more ubiquitous, suggesting a shift toward more widespread commercial applications. Scalable business models will strengthen further growth. There is a substantial increase in global commercial flight hours to 10.8 million in 2024, which is a growth of 42% compared to 2023. Asia continues to be the leading region for drone operations, with around 3.8 million flight hours, followed by Europe and North America.

VLOS and BVLOS Operation

The VLOS mode of operation still dominates (compared to BVLOS), and a considerable increase (up to 61%) was measured in every region worldwide. South America and Oceania showed the most significant increase in VLOS, followed by Europe and the US, which had almost similar flight hours.

BVLOS mode of operation proves to be an ongoing challenge for most countries. Only a handful of countries can scale BVLOS operations so substantially that they can increase the BVLOS share of an entire region (Asia, MEA). Europe and North America show a strong increase in the VLOS mode, but the increase in BVLOS is only in the single digits.

The various national implementations of drone regulations can explain the different growth of BVLOS in different regions. Some countries have more progressive frameworks and support more advanced drone operations. Australia, Norway, and China enable more BVLOS flights through simplified and digital application processes, airspace integration, and close cooperation with the industry. The Drone Regulation Report 2024 provides more details and in-depth country profiles.

Regulation and Adoption Readiness Remain Core Challenges

The infographic and the Global Drone Review 2024 report show a positive trend in utilization and a slight increase in the positivity of expectations. However, many smaller market players struggle with sales and orders alongside a few established brands and service providers.

The biggest challenge is still the over-administrated drone regulation, which, on the one hand, leads to immense compliance costs and, on the other hand, has not yet been able to solve the problem of lengthy approval processes. Drone operators report that for 45% of all applications, the approval process still takes longer than one month – and for 5%, even more than six months.

Operational costs are the second-biggest issue for drone operators. Many end users believe that using drones significantly reduces costs compared to traditional methods. While this has been clearly proven in VLOS operations, BVLOS operations are associated with high, sometimes even higher, costs for maintaining flight safety and expensive equipment and personnel.

Ready to learn more about drone utilization and the market as such? Learn more in the Global Drone Review 2024 Report!

Global Drone Review 2024 Report

• 50-page drone market report featuring:

• Breakdown of market by industry segment

• Data on revenues and exports

• Operational data including number of flights and flight hours

• Company Rankings in 4 Categories

Scalability and its' Current Limitations

Regulators: For the drone market to grow stronger, further improvements in regulation are required. As of today, scalability through standards and regulations is not possible. Regulators often don’t move at the same pace as the industry, offer few solutions, and are hard to convince of suggestions. Regulatory processes remain very individual and labor-intensive, making navigating those frameworks complex and lengthy.

Technology: One way to start scaling a business is to detach from lengthy procedures and “hard-wire” the ability to mitigate strategic and tactical risks into drone and ground control systems. Such sophisticated solutions can help convince the regulator to loosen the reins a little since all the safety procedures (usually 100 pages of risk mitigation procedures) are now baked into the design.

Harmonization: Changing this is easier said than implemented. However, increasing modularity, internal process standardization, and expanding into new markets may fail, especially if drone operation laws still need to be implemented or harmonized internationally.

Costs: Next to regulation and technology, a considerable aspect of pushing the limits is decreasing CapEx and OpEx. Both costs are especially high for advanced operations since many jobs are tailored to a specific task or client. The flexibility offered is good, but the effort to create it might make the whole endeavor unprofitable.

Partnerships: It’s “elbows in” when bundling efforts to market products and services – horizontally, not vertically. Instead of partnering with a company that can provide a component to your business, it’s time to partner with similar companies and bundle the market power and marketing capacity to the industry and regulators.

Greater customer focus, community/partnership building, technological innovations, and adequate revenue models are prioritized most. Strong and trustworthy partners in the same industry help with community building. The Global Drone Review Report 2024 lists the leading global players.

Besides his financial oversight, Hendrik is an expert in aviation law and UAV regulation with more than 10 years of experience. Not only does he consult on all regulation questions, but Hendrik also writes the yearly drone investments report. Prior to launching DRONEII, at Lufthansa Technik he was the single point of contact to Civil Aviation Authorities (CAA) of Germany, Middle East and Asia.