9 min read

When the Rules Run Out: What Recent Developments Reveal About the Regulatory Race in Drone Delivery

Why a European drone delivery company moves to the US

In June 2026, one of Europe’s most active drone delivery operators halted flights in the country that built it. Manna ceased delivery operations in Ireland after Dún Laoghaire-Rathdown County Council refused planning permission for a new aerial delivery hub near Dundrum Town Center, redirecting the company’s growth toward markets abroad. The refusal did not hinge on aviation safety or a lack of drone delivery regulation. It turned on a Noise Impact Assessment the council deemed insufficient — specifically, its reliance on averaged metrics, ill-suited to the intermittent, repetitive character of drone noise — and an Ecological Impact Assessment deemed inadequate with respect to biodiversity.

Manna’s own statement placed the blame on a structural gap: the absence of a clear national framework has left the sector reliant on local planning processes and created uncertainty about the infrastructure needed to support drone delivery at scale. The company, which employs nearly 200 people in Ireland, described its withdrawal as a “strategic pause” and said that local operational hubs in Ireland would not move forward “at this time,” with the focus shifting to the UK, US, and UAE.

Founder and CEO Bobby Healy has rejected claims that Manna is abandoning Ireland — research, development, and manufacturing remain — but the optics are stark: a homegrown company that helped prove drone delivery at scale is now deploying its operational growth capital elsewhere, where it can compound. The key question is not whether Manna left, but why it had to.

A credible company making a rational call

Manna is not a struggling startup grasping for relevance. In April 2026, it closed a $50 million Series B round, has completed well nearly 400,000 commercial deliveries, and claims a positive contribution margin on every flight. Its near-term plan is to open 40 to 50 new US locations over twelve months, starting in Texas and Oklahoma.

Manna now operates in a field that has thinned to a handful of major players like Flytrex, Wing, Zipline, and Amazon Prime Air. When a company with that profile decides where to allocate its next dollar of operational growth, the decision says something about the markets, not just the company. And Manna’s money is moving out of continental Europe, being called “a rational founder making a rational call.”

The European experience can be described as one in which every milestone takes longer than it should and every approval feels like it came despite the system rather than because of it. The point is not that Europe cannot lead, but that European operators are increasingly forced to ask whether to keep making the harder bet.

The US unlock? The potential of FAA Part 108

The reason investors are moving now is regulatory. Historically, the FAA required drone operators to keep aircraft within visual line of sight, making commercial delivery at scale effectively impossible without a one-off waiver for every flight. In August 2025, the agency published the Part 108 NPRM — a proposed permanent ruleset that would normalize beyond-visual-line-of-sight (BVLOS) operations using performance-based standards rather than traditional type certification. The final rule was expected in spring 2026, driven by a 240-day deadline set in a June 2025 executive order on drone policy.

This is the “unlock” that the financing reflects: a clear, permanent, nationwide pathway to fly BVLOS without bespoke approvals.

But two cautions belong here: First, the rule is not yet final. The NPRM drew more than 3,000 comments, the FAA reopened the comment period into 2026, and implementation will likely take six to twelve months after publication. A view worth airing — raised in reader commentary on the NPRM and consistent with the European experience — is that the optimism may be premature: a rule is only as fast as its implementation, and someone has to process the risk assessments. If the FAA does not build up the staff to handle that workload, US BVLOS authorizations could prove as slow in practice as Europe’s, regardless of how clean the framework looks on paper.

The second caution is more interesting because it is already happening.

THE 9th GLOBAL DRONE INDUSTRY SURVEY

Share your wisdom – the industry is listening!

After 9 years and thousands of voices, it is time to update the FREE WHITE PAPER that moves the drone industry.

The insights you share in the next 10 minutes will end up cited in boardrooms, policy papers, and investment decks worldwide – perhaps your own.

Participate now for a chance to win attractive prizes!

The US workaround: registering drones as aircraft

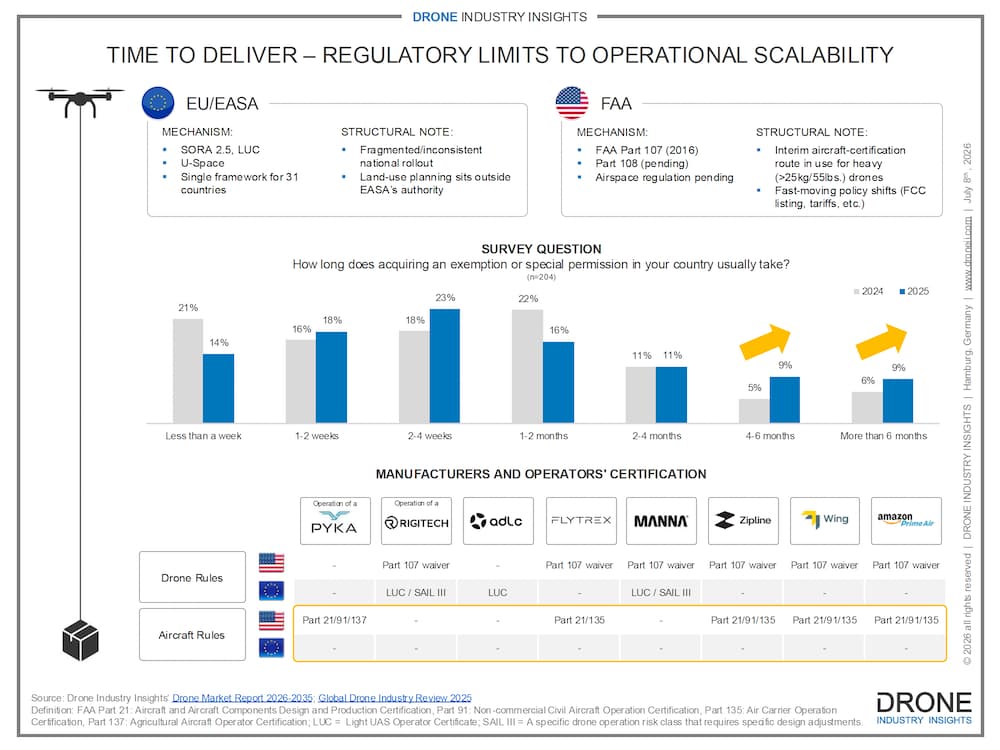

While Part 108 is pending, a notable trend has emerged among US operators of heavier drones (over 55 lbs./25 kg): rather than wait for the immature BVLOS rules, they treat the drone as a conventional aircraft. The drone is entered in the FAA aircraft register, receives an N-registration, and either an airworthiness certificate or a Section 44807 determination. Afterward, the FAA regulates it much like a crewed aircraft — easing integration into controlled airspace and making BVLOS authorizations more attainable. Examples of typical regulatory pathways – or workarounds – can be found in this infographic.

The practical effect is that, until Part 108 is established, the FAA is steering large drones away from Part 107 and toward the traditional aircraft certification and operating framework. FAA guidance confirms the mechanics: Part 135 is currently the only path for small drones to carry another party’s property for compensation BVLOS; drones over 55 lbs. fall under Part 91 with exemptions; and an N-number plus an airworthiness determination is the route to operate them. It is not “bypassing immature drone rules”; it is the FAA’s established heavy-drone pathway, instead of a loophole.

This matters for the EU comparison: it shows the US has a functioning interim route to scale even before its dedicated BVLOS rule takes effect. Europe has no equivalent single shortcut: its main self-authorization route, the LUC, has a high threshold, and authorizations don’t transfer reliably across borders.

Europe is more capable than the binary suggests

It would be easy and wrong to read this as “EU bad, US good.” Europe’s drone regulation is mature and, in some respects, ahead. EASA adopted SORA 2.5 in September 2025, introducing a more quantitative ground-risk model, clearer criteria that reduce national interpretation, and simplified authorization for lower-risk operations. The continent is also rolling out U-space, its digital airspace management framework for routine BVLOS. Crucially, a single EASA framework opens the door to 31 countries — the 27 EU member states plus Norway, Iceland, Switzerland, and Liechtenstein — rather than one.

Manna itself is evidence that the airspace rules are not the wall. The company has operated in Ireland for seven years under the supervision of the national aviation authority. The regulator cleared Manna to fly. Something else stopped it.

Global Drone Market Report 2026-2035

- Extensive 244-page drone market report with in-depth analysis, industry definitions, & extended 10-year forecast.

- Market Size broken down

- by Recreational & Commercial

- by Industry Segment (hardware, software, services)

- by Application Method (Mapping, Inspection, etc.)

- by Unit Sales

- by Region and Country

- Market Developments and Trends

- Drone Regulation

- Drone Investments

- Drone Company Market Shares

Where Europe actually breaks down

The European problem sits in two places, and neither is the airspace framework itself.

The first is fragmentation. Europe applies a supposedly harmonized framework through fragmented national lenses, so a concept proven in one country is not automatically portable to another. For an operator, every national border can feel like a regulatory reset — with duplicated work, duplicated uncertainty, and slower cross-border scaling. SORA 2.5 narrowed the room for interpretation, but it did not dissolve the national boundaries governing how authorizations are granted and recognized.

The second, and the one that grounded Manna, is the gap between aviation approval and the right to operate on the ground. Clearing the airspace bar does not grant land-use permission. Planning and zoning fall to member states and, ultimately, local councils — entirely outside EASA’s reach. Manna’s Dundrum hub was refused not by an aviation regulator but by a county council, on noise and ecological grounds, with decisions made “case by case, hub by hub.” That is where the genuine US–EU contrast lies: not in the sophistication of the airspace rules, but in fragmented national implementation and a local-planning layer that no aviation regulator controls — and, as the US workaround shows, in the absence of a functioning interim route to scale while the dedicated rules mature.

What it means for the business - and the alternatives

For operators and investors, the lesson is that the first-mover advantage is shifting toward jurisdictions that offer end-to-end clarity, from airspace down to the launch pad. Capital follows a predictable path to scale, and that path is clearer outside continental Europe right now.

Three markets illustrate where near-term momentum is pooling, and they are precisely the ones Manna named. The UK’s Civil Aviation Authority has a roadmap targeting routine BVLOS operations around 2027 and operates its own SORA-based digital application platform. The US, despite Part 108 still being pending, offers both a credible timeline and the interim aircraft-certification route described above. China is tightening airworthiness certification from July 2026 while pushing hard for commercial deployment. Manna already holds or is pursuing operational authorizations across these markets — which is why they are absorbing its growth.

The UAE stands in sharp contrast to the European picture. Healy himself singles it out: in his words, “UAE (via GCAA and DCAA) has excellent fully-baked regulations and has solved the airspace access also.” Drone operations are indeed governed by a codified federal framework (Federal Decree-Law No. 26 of 2022, implemented through the GCAA’s CAR-UAS rules) with the Dubai Civil Aviation Authority (DCAA) providing emirate-level oversight, with drones treated legally as aircraft. Critically for the airspace question, the GCAA operates a national UTM system and a layered vertical airspace design that reserves 0–500 ft as a managed drone-operations zone for delivery and inspection flights — the same integration problem Europe leaves to fragmented national and local processes is handled centrally here. What the UAE demonstrates is a single authority owning airspace and the route to operate in it — precisely the end-to-end clarity Europe lacks.

The counterpoint deserves equal weight. Europe’s more structured entry path also tends to reward operators who invest early in compliance: higher margins, lower saturation, and a single qualification that, once earned, applies across a continent. The barrier and the moat are the same wall, seen from different sides — and some European operators are choosing to keep building precisely because they expect that wall to come down.

A case study, not a verdict

Manna’s pause is best read as a data point on regulatory systems, not a referendum on any one country. The technology is ready; the planning consensus and cross-border implementation needed to scale it are not yet in place in Europe. Even the US advantage is qualified — its dedicated BVLOS rule is unfinished, its interim path leans on decades-old aircraft regulation, and its speed will ultimately depend on administrative capacity. The competition in drone delivery is increasingly between regulatory regimes — how quickly and how completely they convert technical readiness into permission to operate — as much as between the companies flying under them. Where that race is won will shape where the next 400,000 deliveries take off.

Named one of the most influential people in the commercial drone industry, Kay established Drone Industry Insights as the leading drone market research consultancy in 2015. As well as personally consulting on projects and producing reports, he frequently speaks at conferences, seminars, and expos.

- 1 A credible company making a rational call

- 2 The US unlock? The potential of FAA Part 108

- 3 The US workaround: registering drones as aircraft

- 4 Europe is more capable than the binary suggests

- 5 Where Europe actually breaks down

- 6 What it means for the business - and the alternatives

- 7 A case study, not a verdict