6 min read

Dual-use Drones Dominate Global Funding: Drone Investments Reached a Record High in 2025.

Dual-use Drones Drove Record Drone Funding of USD 3.86 Billion in 2025.

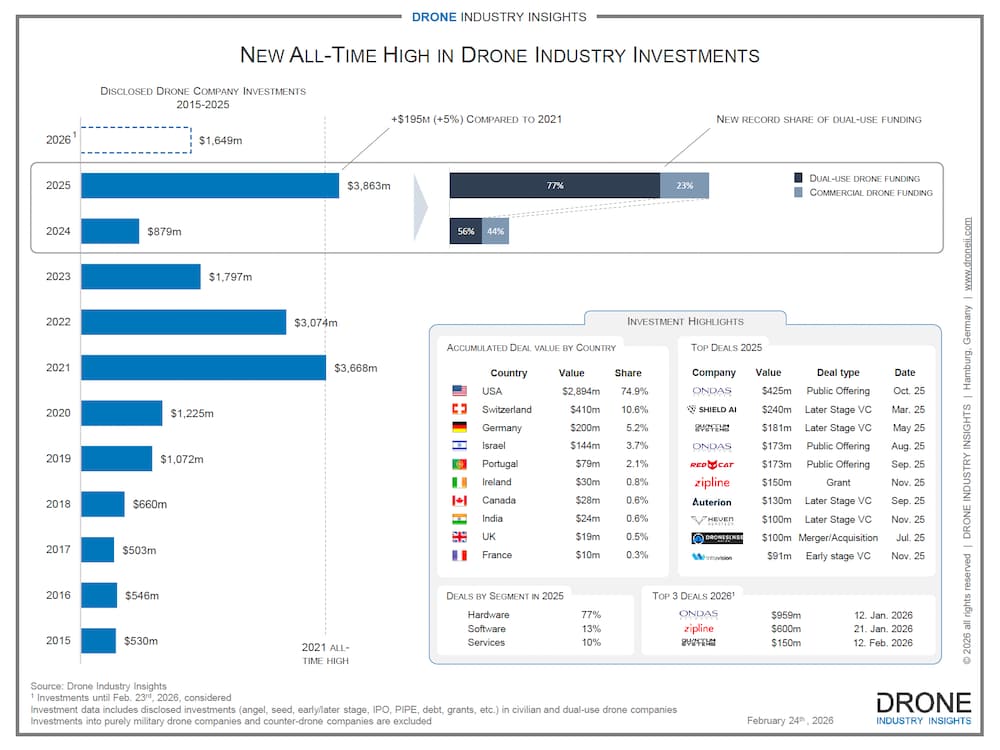

At USD 3.86 billion, the commercial drone market set a new investment record in 2025, surpassing the previous high of USD 3.67 billion in 2021. After a sharp decline in recent years (down 42% in 2023 to USD 1.79 billion and down another 52% in 2024 to USD 879 million), the recovery is impressive, driven by a shift toward a dual-use drone market.

In one of last year’s published articles, it was already anticipated that the markets would rebound from the “trough of disillusionment” in 2025, and that expectation has now materialized in the most dramatic form.

But celebrating the figures alone is not enough. Behind the record lies an industry in transition, with new drivers, capital structures, and geographic focal points. This article analyzes the central narratives behind the figures and asks: What does this mean for investors and drone companies?

Dual-Use Drones Dominate the Investment Landscape. But What Exactly Does That Mean?

The most important finding is that 77% of the total investment went to companies focused on dual-use drones, i.e., those that address both civilian and military applications. The commercial drone market alone raised only 23% ($888m) of this record total, which, however, is still more than twice the 2024 total.

Today, the term “dual-use drones” describes less of a distinct category and more of a broad spectrum of strategic positioning. Drone companies that serve consumer, civil, and government markets in addition to military customers are often classified as dual-use across the board, regardless of the actual defense share of their business.

The last few years have seen the start of a significant shift from civilian to defense drone use.

Regulatory breakthroughs necessary for broader commercial adoption (such as standardized BVLOS rules in the EU or the US) are still not in sight. Therefore, some drone companies, which originally started as consumer and commercial drone manufacturers, had to reposition themselves to address the governmental and military markets. Their main customers today include police forces, Homeland Security, and the DoDs of the world, which was unthinkable just a few years ago.

There are basically two different types of dual-use drone companies. There are companies with a deliberate parallel strategy across the civil and military markets, often using platforms that are partially identical. These companies actively invest in both sales channels and both certification paths. Then there are those that pivoted a while ago or just pivoted and look back on a civil heritage but focus on governmental/military use (more or less) exclusively today.

This shows that the industry is not experiencing a homogeneous wave of dual-use drones but rather different strategic (and sometimes opportunistic) responses to the same geopolitical reality.

Drone Investments Database 2015-2025

- 1657 drone investments from 2015-2025

- Across all sectors: hardware, software, and services

- Separation by deal types (angel, seed, early/later stage, IPO, PIPE, etc.)

- Additional 82 counter-drone deals

- List of 3507 corresponding investors

Hardware is on the Rise Again, But This Time it's a Different One.

Another noteworthy finding: 77% of investments went to hardware companies (2023: 46%, 2024: 70%). This stands in stark contrast to the software-first trend of previous years, when platforms, data services, and autonomous software solutions dominated investor attention.

The explanation is simple: new military requirements for design and function make large numbers of drones necessary, and this, combined with a new economy, is driving mass production – a combination defense primes are not used to.

The ability to scale up mass production has become a strategic imperative. It is no coincidence that industrial giants such as Bosch, Renault, Aumovio (formerly Continental), and Motorola are increasingly moving toward drone mass production and focusing on establishing national supply chains.

This does not spell the end for software-driven business models, but it does send a clear message: companies that cannot demonstrate a compelling hardware foundation are currently finding it more difficult to raise capital.

New Financing Structures: Capital Increases as a Sign of Maturity

In addition to shifts in content, there has been a noticeable structural change in financing: capital increases (hardly an issue in the boom years before 2022) became an important instrument of corporate financing in 2025.

The value of public offerings increased from 2023: 0% to 2024: 2% to 2025: 24%.

This sign of market maturity shows that it’s no longer young startups raising fresh venture capital, but rather established companies growing and scaling through capital raises. This development signals two things: First, that part of the industry has actually survived the chasm. Second, investors are willing to invest in proven business models with demonstrated traction rather than primarily in promises.

But there is more: Ecosystems and supply chain rigidity are key in a military context. Some drone manufacturers, such as Quantum Systems, RedCat, and ONDAS Inc., are making targeted investments in specific companies within their own supply chains to pursue vertical integration as a competitive strategy. It is a clear sign that some players have outgrown the start-up phase and are actively seeking leverage and control over their value chain.

Geography: America Investors Dominate, Germany Surprisingly Ranks Second

Geographically, the picture is predictable but nevertheless revealing. US companies received 70% of the total investment. This was facilitated by the vibrant US capital markets, where numerous public offerings took place. For European and Asian players, the structural disadvantage in access to capital therefore remains.

Another finding is even more surprising: measured by the number of investors, Germany ranks second worldwide with a 10% share, behind the US with 40%. This figure does not reflect the amount invested but shows how actively and broadly German capital is involved in the global drone market. Behind this figure lies a wide range of motives. German venture capital funds account for the largest share, continuing to invest in the sector despite the difficult years that preceded them. In addition, corporations are making strategic investments to secure access to technology and strengthen supply chains.

Summary and Outlook: Signs Point Towards Continuation

The key question is whether 2025 marked the beginning of a sustainable upswing – or an outlier driven by geopolitics and stock market hype. The initial data from 2026 is encouraging. In the first two months of the year alone, around $1.7 billion was invested in the drone market. Extrapolating, this would mean an annual volume that could once again exceed the record set in 2025.

The composition of this investment is particularly significant: these investments are flowing not only into dual-use drones and defense applications in general, but also into the purely civilian market. The most prominent example is Zipline, the international drone delivery company that raised $600 million in a later-stage VC round. This is an encouraging signal: investors once again show confidence in the commercial potential of drones beyond the battlefield.

Besides his financial oversight, Hendrik is an expert in aviation law and UAV regulation with more than 10 years of experience. Not only does he consult on all regulation questions, but Hendrik also writes the yearly drone investments report. Prior to launching DRONEII, at Lufthansa Technik he was the single point of contact to Civil Aviation Authorities (CAA) of Germany, Middle East and Asia.

- 1 Dual-Use Drones Dominate the Investment Landscape. But What Exactly Does That Mean?

- 2 Hardware is on the Rise Again, But This Time it's a Different One.

- 3 New Financing Structures: Capital Increases as a Sign of Maturity

- 4 Geography: America Investors Dominate, Germany Surprisingly Ranks Second

- 5 Summary and Outlook: Signs Point Towards Continuation