6 min read

Drone Market Map 2026: 1413 Companies, 70 Countries, One Industry

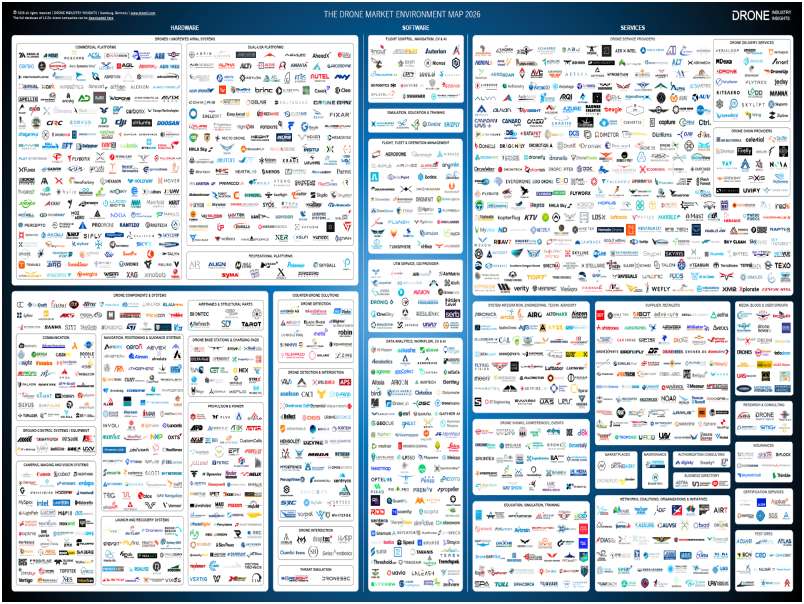

Drone Market Map 2026: 1,413 Drone Industry Companies in One Infographic

The Drone Market Map 2026 features 1,413 companies from 70 countries in the drone industry across hardware, software, and services — a 31% increase over the 1,076 companies listed on the last edition. The map has not been updated since 2022, and over the past four years, the global drone ecosystem has undergone a structural transformation. New categories have been added, the balance among segments has shifted, and an entirely new segment has emerged.

How Many Companies Are on the Drone Market Map 2026?

The 2026 edition lists 1,413 companies. Approximately 300 companies from the 2022 edition have been removed due to mergers, acquisitions, bankruptcies, or pivots out of the civil drone sector. At the same time, roughly 637 new companies have been added, resulting in a net increase of 337 entries. The drone industry continues to churn — but it is growing faster than it is consolidating.

As with every edition, it must be stated: these are not all the drone companies in the world. The map is physically limited in size. The inclusion or exclusion of any company should not be interpreted as an endorsement or judgment. What the Drone Market Map 2026 offers is a structured, visual overview of the global drone ecosystem’s diversity and direction.

How Is the Drone Market Segmented in 2026?

The balance among the three main segments on the map has changed compared to 2022.

Hardware still accounts for the largest share at 46% (644 companies), down from 49.5% in 2022. Services have grown from 37.6% to 42% (592 companies). Software remains the smallest segment at 12% (177 companies).

The three largest sub-segments are Drone Service Providers (302), Platform Manufacturers (295), and Components & Systems (285), and together represent more than 60% of all companies on the map. As drones become increasingly commoditized and put to work, value is shifting downstream to operations, integration, data analytics, and consulting.

THE 9th GLOBAL DRONE INDUSTRY SURVEY

Share your wisdom – the industry is listening!

After 9 years and thousands of voices, it is time to update the FREE WHITE PAPER that moves the drone industry.

The insights you share in the next 8–15 minutes will end up cited in boardrooms, policy papers, and investment decks worldwide – perhaps your own.

Participate now and have the chance to win attractive prizes!

What Is the Dual-Use Drone Shift?

The most consequential development since 2022 is the strengthening of the dual-use sector.

The war in Ukraine has fundamentally altered how drones are perceived and deployed in modern conflict, demonstrating that inexpensive, commercial-grade systems can have an outsized impact on the battlefield. But the effect on the broader industry extends far beyond the conflict itself.

Record defense spending across NATO and allied nations, driven by the urgency of building domestic drone and counter-drone capabilities, has created a powerful pull on the commercial sector. For many companies that have been struggling to find sustainable business models in the commercial market, where regulatory limitations remain the single biggest obstacle to widespread adoption, this wave of public defense funding has opened an alternative revenue path.

The result is a growing number of companies pivoting toward dual- or triple-use, serving commercial, public safety, and defense customers from a single technology stack. Notably, purely military drone manufacturers are not included in the Drone Market Map 2026. Ukrainian companies, for instance, are largely absent because their systems are currently almost entirely military. The map highlights this commercial-to-dual-use pivot, which represents a structural change in reshaping the competitive landscape in real time.

What New Sub-Segments Were Added in 2026?

Several new categories reflect both the dual-use shift and the broader maturation of the drone ecosystem.

Counter-Drone Systems: Threat Emulation. As NATO countries invest in counter-drone defense systems, realistic drone threats are needed for testing and training— creating an entirely new niche that barely existed in 2022.

Drone Hardware: Airframes & Structural Parts, and Drone Base Stations & Charging Pads. The emergence of dedicated airframe suppliers and improved drone infrastructure providers signals that a highly specialized supply chain is taking shape, representing a hallmark of industrial maturity.

Services: Authorization Consulting, Certification Services, and Business Directories. These additions underscore that regulatory complexity is not only a barrier to adoption but can also be a business. Authorization Consulting helps operators navigate approval processes; Certification Services refers to organizations that grant those approvals; and Business Directories connect drone companies with customers along the supply chain.

Global Drone Market Report 2026-2035

- Extensive 244-page drone market report with in-depth analysis, industry definitions, & extended 10-year forecast.

- Market Size broken down

- by Recreational & Commercial

- by Industry Segment (hardware, software, services)

- by Application Method (Mapping, Inspection, etc.)

- by Unit Sales

- by Region and Country

- Market Developments and Trends

- Drone Regulation

- Drone Investments

- Drone Company Market Shares

Where Are Most Drone Industry Companies Located?

On the Market Map, the United States remains the leader with 454 companies (about 32%), up from 337 in 2022. Germany ranks second with 100 companies, followed by Canada (87), the United Kingdom (78), and China (63). France (59), Switzerland (56), and Australia (51) round out the top eight.

The geographic distribution skews heavily toward North America and Europe. Asia, while home to some of the world’s largest drone manufacturers by revenue and market share, is represented by fewer but often significantly larger companies.

What Are the Limitations of the Drone Market Map?

The Drone Market Map 2026 includes companies across hardware, software, and services — spanning hobby, commercial, and dual-use applications. As mentioned earlier, manufacturers that build platforms exclusively for the military market are excluded. The map is also constrained by size: with more than 1,400 logos already featured, not every company in the drone industry can be represented.

Named one of the most influential people in the commercial drone industry, Kay established Drone Industry Insights as the leading drone market research consultancy in 2015. As well as personally consulting on projects and producing reports, he frequently speaks at conferences, seminars, and expos.